This is one of several articles that we’ll feature on long-term care insurance. You’ve heard about it, you may know something about it, somebody may have tried to sell it to you, but you really never understood it or why it may (or may not) be a good idea for you.

Many reading this are Boomers, like myself. The Boomer generation is generally defined as those born between 1946-1964. Even if you are of the pre-Boomer generation (The “Traditionalists” or “The Silent Majority”), you lived through all that defined the Boomer generation, including:

- The popular music and clothing of the time

- The breaking down of old traditions and creation of new traditions

- The sexual revolution

- Anti-war protests

- Increased longevity

Check out this interesting chart outlining some of the characteristics of now-living generations.

Also read our post What Is Long-Term Care and Who Might Need It?

The first five points above were probably fun for most of us (each in their own way). Let’s call them the “loud” characteristics of being a Boomer: Concerts, trashing old traditions, forging new trails, creating fashion trends, openly acknowledging the fun-value of sex (as opposed to mainly for procreation), and speaking one’s mind about armed conflict.

But the last one, increased longevity, while better than the alternative, has implications that not all of us foresaw.

The Conundrum of Longevity

Boomers include people who are 55-65. Let’s use that range as our example; it happens to also encompass the age that many individuals want to retire (65). According to data compiled by the Social Security Administration:

- A man reaching age 65 today can expect to live, on average, to age 84.3 (almost 20 more years).

- A woman turning age 65 today can expect to live, on average, to age 86.8 (almost 22 more years).

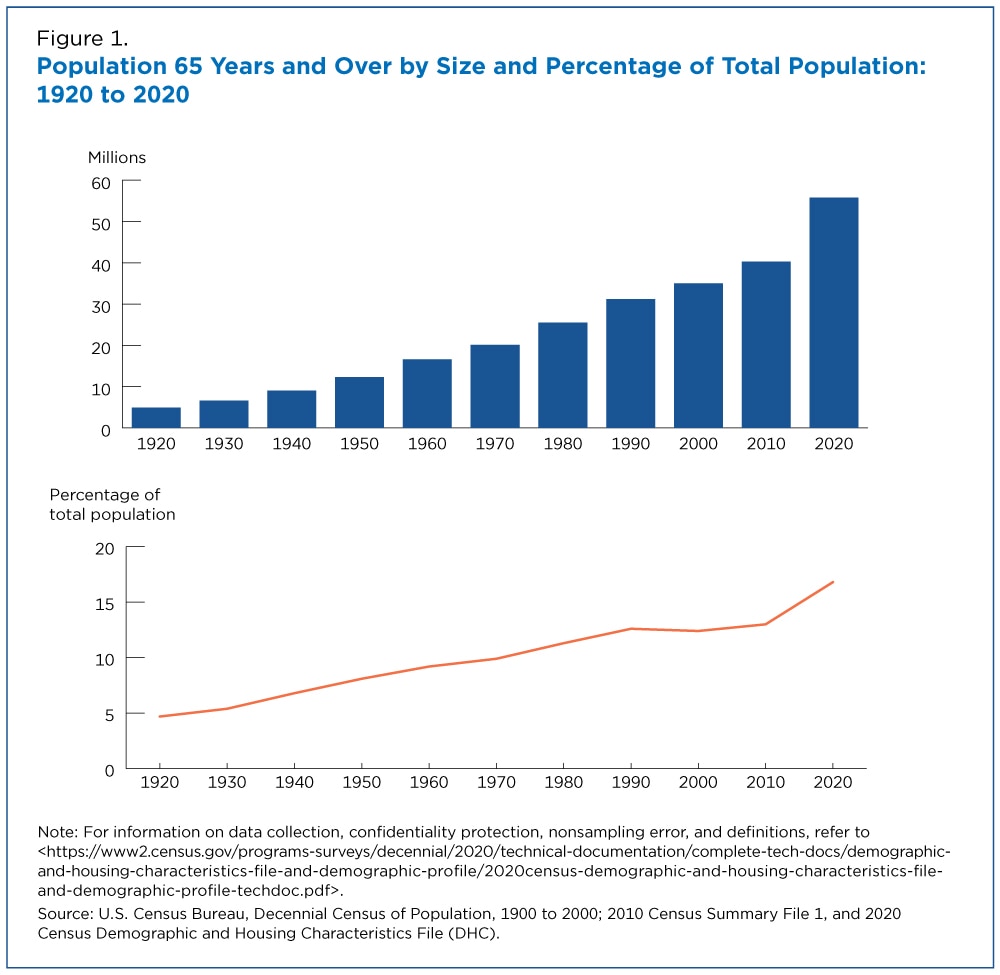

- According to the 2020 census, one in 6 people in the US were 65 and older.

- Citing data from the New York Life Wealth Watch survey in 2023, baby boomers have an average of $223,498.27 in retirement savings. That translates into about $8,940 in annual post-retirement income (excluding income from Social Security). Applying the widely used 4% rule of retirement, that would mean that a savings nest egg of about $2,158,345.91 is needed at age 65 today. That doesn’t even consider the “outliers” who live to 90, 95, or even to 100.

{kind=link}

How Does Long-Term Care Insurance Fit In?

One of the big problems with longevity is money to finance it; or, more specifically, the lack thereof. A reality of longevity is that health issues arise. Not all health expenses are covered by private insurance if you still have it, Medicare, prescription coverage, Medicare Supplements, or Medicare Advantage plans. You will still have to pay premiums, co-payments, and deductibles. There will also be expenses that are disallowed or only partially covered, making them your financial responsibility.

All of that assumes that you remain pretty healthy and able to take care of yourself (maybe with some family help). If your physical or mental health declines to the point that you can’t be independent, or family help isn’t available, you may have to consider long-term health insurance. Ideally, you considered it before the need arose (because you won’t be able to get it after). We’ll discuss the specifics of long-term care insurance in later articles.

(This article has been updated since it originally appeared June, 2016.)